Featured

Table of Contents

Insurance provider won't pay a small. Rather, think about leaving the cash to an estate or trust fund. For even more in-depth details on life insurance policy get a duplicate of the NAIC Life Insurance Policy Purchasers Guide.

The internal revenue service puts a limitation on just how much cash can enter into life insurance costs for the policy and just how quickly such costs can be paid in order for the plan to retain all of its tax obligation advantages. If specific limits are exceeded, a MEC results. MEC policyholders may be subject to tax obligations on circulations on an income-first basis, that is, to the extent there is gain in their policies, as well as penalties on any type of taxable amount if they are not age 59 1/2 or older.

Please note that exceptional fundings build up passion. Revenue tax-free treatment additionally presumes the lending will become satisfied from revenue tax-free fatality advantage earnings. Finances and withdrawals reduce the policy's cash money worth and death advantage, might trigger specific policy benefits or cyclists to end up being not available and may boost the possibility the policy may lapse.

A client might qualify for the life insurance, but not the cyclist. A variable global life insurance agreement is an agreement with the primary objective of supplying a death advantage.

What should I look for in a Cash Value Plans plan?

These profiles are closely taken care of in order to satisfy stated investment purposes. There are charges and costs related to variable life insurance policy contracts, including death and danger fees, a front-end tons, administrative fees, investment management charges, abandonment charges and charges for optional riders. Equitable Financial and its associates do not give lawful or tax guidance.

Whether you're beginning a household or marrying, individuals normally start to consider life insurance policy when another person begins to rely on their capability to make an income. Which's great, since that's precisely what the death benefit is for. As you discover a lot more regarding life insurance coverage, you're most likely to locate that many plans for circumstances, whole life insurance policy have a lot more than simply a death benefit.

What are the benefits of entire life insurance coverage? One of the most enticing benefits of purchasing an entire life insurance coverage plan is this: As long as you pay your premiums, your death benefit will certainly never ever expire.

Assume you do not need life insurance policy if you don't have children? There are lots of benefits to having life insurance, also if you're not supporting a family.

Riders

Funeral expenses, funeral costs and medical costs can include up (Long term care). The last thing you desire is for your loved ones to carry this additional concern. Irreversible life insurance is offered in various amounts, so you can select a survivor benefit that satisfies your requirements. Alright, this one only applies if you have youngsters.

Establish whether term or irreversible life insurance policy is ideal for you. Then, obtain a price quote of exactly how much protection you may require, and exactly how much it could set you back. Discover the correct amount for your budget plan and assurance. Locate your amount. As your individual scenarios modification (i.e., marital relationship, birth of a youngster or task promo), so will your life insurance policy needs.

Generally, there are 2 types of life insurance plans - either term or irreversible strategies or some combination of both. Life insurance companies use different forms of term strategies and conventional life policies along with "rate of interest delicate" items which have actually become a lot more widespread considering that the 1980's.

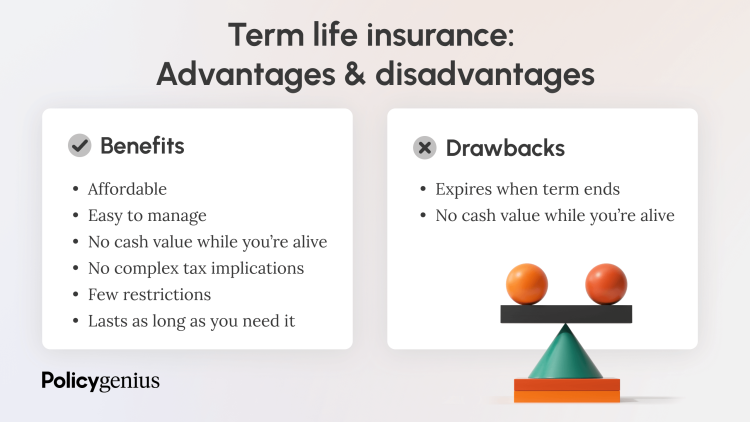

Term insurance coverage offers defense for a specific amount of time. This duration could be as short as one year or provide insurance coverage for a certain variety of years such as 5, 10, two decades or to a specified age such as 80 or in many cases up to the earliest age in the life insurance coverage mortality tables.

Who offers flexible Senior Protection plans?

Presently term insurance coverage rates are extremely competitive and amongst the most affordable historically skilled. It should be kept in mind that it is a widely held belief that term insurance is the least expensive pure life insurance policy protection offered. One requires to assess the plan terms thoroughly to choose which term life options are suitable to meet your specific conditions.

With each new term the costs is raised. The right to renew the policy without proof of insurability is a vital advantage to you. Otherwise, the danger you take is that your health may degrade and you might be not able to obtain a policy at the exact same prices and even at all, leaving you and your recipients without coverage.

The length of the conversion duration will vary depending on the kind of term policy acquired. The costs rate you pay on conversion is generally based on your "present acquired age", which is your age on the conversion date.

Under a degree term policy the face quantity of the policy continues to be the same for the whole duration. Usually such plans are sold as mortgage protection with the quantity of insurance reducing as the equilibrium of the mortgage reduces.

Who offers Income Protection?

Generally, insurers have not deserved to transform premiums after the plan is marketed. Because such plans may proceed for years, insurance providers need to use conservative death, rate of interest and cost rate quotes in the premium calculation. Flexible premium insurance, nevertheless, allows insurance providers to offer insurance policy at reduced "present" premiums based upon much less conventional assumptions with the right to transform these premiums in the future.

While term insurance coverage is made to offer protection for a defined amount of time, permanent insurance is created to offer coverage for your entire lifetime. To keep the premium rate level, the premium at the younger ages goes beyond the actual price of protection. This extra premium develops a get (money worth) which aids pay for the policy in later years as the cost of defense surges above the costs.

The insurance firm spends the excess premium dollars This type of policy, which is occasionally called cash money worth life insurance coverage, creates a financial savings element. Money values are critical to a permanent life insurance coverage plan.

{kind=link}

Latest Posts

Best Life Insurance For Funeral Expenses

Final Coverage

Instant Universal Life Insurance Quotes