Featured

Table of Contents

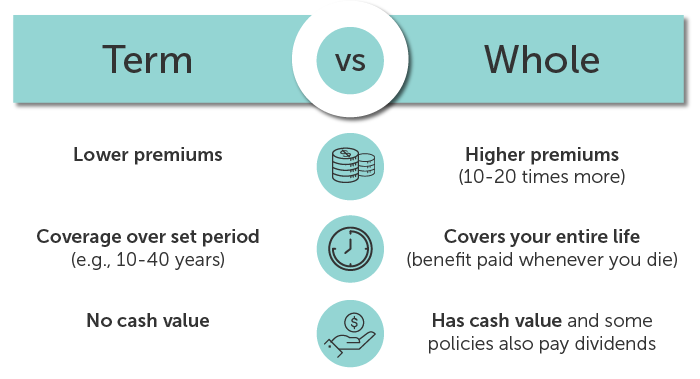

Level term life insurance coverage is among the most affordable protection choices on the marketplace because it supplies basic defense in the form of fatality benefit and only lasts for a set amount of time. At the end of the term, it ends. Entire life insurance policy, on the other hand, is dramatically extra pricey than degree term life due to the fact that it does not run out and features a cash money value function.

Rates may differ by insurance company, term, coverage quantity, health class, and state. Level term is an excellent life insurance policy alternative for the majority of people, however depending on your coverage requirements and individual circumstance, it could not be the best fit for you.

What should I look for in a Level Death Benefit Term Life Insurance plan?

This can be an excellent alternative if you, for instance, have simply quit smoking and require to wait 2 or three years to apply for a degree term policy and be eligible for a lower rate.

, your death benefit payment will certainly decrease over time, however your settlements will remain the same. On the other hand, you'll pay even more in advance for less protection with an increasing term life policy than with a degree term life policy. If you're not certain which kind of plan is best for you, working with an independent broker can aid.

Level Death Benefit Term Life Insurance

Once you have actually decided that degree term is ideal for you, the next step is to acquire your policy. Below's how to do it. Calculate just how much life insurance coverage you require Your coverage amount need to give for your household's lasting economic requirements, consisting of the loss of your earnings in case of your death, along with debts and daily expenses.

As you search for methods to secure your monetary future, you've likely stumbled upon a wide array of life insurance alternatives. Choosing the ideal insurance coverage is a big decision. You wish to discover something that will certainly help sustain your enjoyed ones or the reasons crucial to you if something happens to you.

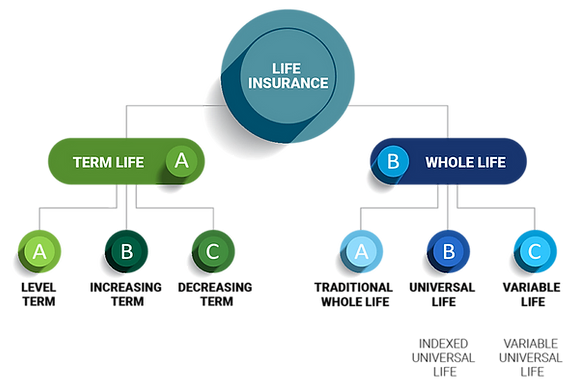

Several people lean toward term life insurance policy for its simplicity and cost-effectiveness. Term insurance contracts are for a reasonably brief, defined amount of time yet have alternatives you can customize to your requirements. Specific benefit options can make your costs alter in time. Degree term insurance policy, nonetheless, is a kind of term life insurance policy that has constant settlements and an imperishable.

What is Level Term Life Insurance Premiums?

Degree term life insurance policy is a subset of It's called "level" due to the fact that your premiums and the advantage to be paid to your liked ones stay the same throughout the agreement. You won't see any type of adjustments in expense or be left asking yourself concerning its worth. Some agreements, such as annually eco-friendly term, may be structured with premiums that boost in time as the insured ages.

They're established at the beginning and continue to be the exact same. Having consistent repayments can help you much better plan and budget plan because they'll never ever transform. Low cost level term life insurance. Dealt with survivor benefit. This is additionally established at the start, so you can understand exactly what survivor benefit amount your can anticipate when you pass away, as long as you're covered and up-to-date on costs.

Level Term Life Insurance Vs Whole Life

You concur to a set costs and fatality advantage for the duration of the term. If you pass away while covered, your death advantage will certainly be paid out to liked ones (as long as your costs are up to day).

You may have the alternative to for an additional term or, most likely, renew it year to year. If your agreement has actually a guaranteed renewability provision, you might not need to have a new medical examination to keep your coverage going. Nevertheless, your premiums are most likely to raise because they'll be based upon your age at renewal time. Best value level term life insurance.

With this alternative, you can that will certainly last the rest of your life. In this instance, once more, you may not need to have any brand-new clinical examinations, however premiums likely will climb as a result of your age and new coverage. Different companies provide different alternatives for conversion, be sure to recognize your choices before taking this step.

Talking to a financial expert likewise may help you identify the course that aligns finest with your general strategy. The majority of term life insurance policy is level term throughout of the agreement duration, but not all. Some term insurance coverage may come with a costs that enhances with time. With reducing term life insurance coverage, your death advantage goes down with time (this kind is often taken out to particularly cover a long-lasting financial debt you're repaying).

What happens if I don’t have No Medical Exam Level Term Life Insurance?

And if you're set up for sustainable term life, then your premium likely will increase yearly. If you're discovering term life insurance policy and intend to make certain simple and predictable financial defense for your family, level term may be something to consider. As with any kind of type of protection, it might have some restrictions that do not satisfy your demands.

Normally, term life insurance coverage is extra budget friendly than irreversible protection, so it's a cost-efficient way to safeguard financial defense. At the end of your agreement's term, you have several choices to continue or move on from protection, typically without needing a clinical exam (20-year level term life insurance).

What types of Level Term Life Insurance Rates are available?

As with various other kinds of term life insurance coverage, as soon as the contract finishes, you'll likely pay higher costs for coverage since it will recalculate at your current age and health. Level term supplies predictability.

That doesn't indicate it's a fit for everybody. As you're buying life insurance policy, below are a few essential variables to take into consideration: Budget plan. Among the advantages of level term insurance coverage is you understand the cost and the survivor benefit upfront, making it easier to without stressing over increases in time.

Age and health. Usually, with life insurance policy, the healthier and younger you are, the much more inexpensive the coverage. If you're young and healthy and balanced, it may be an appealing option to lock in reduced costs now. Financial responsibility. Your dependents and financial responsibility play a duty in determining your coverage. If you have a young family members, as an example, level term can help offer monetary assistance throughout essential years without spending for insurance coverage longer than needed.

{kind=link}

Latest Posts

Best Life Insurance For Funeral Expenses

Final Coverage

Instant Universal Life Insurance Quotes